NEW DELHI: According to 99acres.com report, with the improving home buying sentiment, backed by a widened negotiation window and competitive home loan interest rates, home sales improved by 50 percent in Oct-Dec 2020 vis-à-vis Jul-Sep 2020.

99acres.com Insite is a quarterly report focusing on capital and rental price trends in the residential realty market across eight major cities of India.

The resale segment continued reporting a few distressed deals; however, prices in the primary market remain unchanged. Demand from NRI buyers went up significantly. The rental landscape, however, remained grim as students and working professionals continued operating from their hometowns amid the COVID scare.

Speaking on the report, Maneesh Upadhyaya, Chief Business Officer, 99acres.com, averred, “Amid the turbulence created by COVID-19 pandemic, RBI and GOI announced several measures to aid economic revival. Bringing down home loan interest rates to almost a 15-year-low, stamp duty reductions in Maharashtra and Karnataka, liquidity infusion measures, one-time restructuring of loans and supportive stance for NBFCs, MSMEs, and real estate sector comforted businesses and individuals. With gradual unlocking of cities and news around possible vaccinations, normalcy started returning to the market. This all cumulatively helped push housing demand up and the last quarter of the year recorded a marked improvement in sales against the previous ones. Notably, Delhi NCR, Mumbai, Pune, Bangalore and Chennai reported a 10-45% rise in property sales in Oct-Dec 2020 against Jul-Sep 2020. Improved seller confidence in the market was also evident from a 15 percent rise in owner sale listings posted on 99acres in the same period.

With the infection rate reducing and vaccination drives starting across the country, the worst seems to be behind us and the subsequent revival in businesses, and individual home ownership appetite are likely to aid realty growth in 2021.”

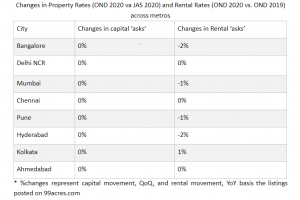

Market Indicators

Confronting the adversities posed by the world health crisis during Apr-Jun 2020, the onset of the final quarter of 2020 seemed promising. A perceptional and behavioral shift, coupled with the renewed housing demand, spiraled into rigorous absorption of housing units in Oct-Dec 2020.

The festive vigour helped developers see improvement in new home sales, which numbered around 21,800 units, up by almost 50 percent, QoQ. Mumbai remained the largest contributor (23 percent) to the overall home sales in Oct-Dec 2020, followed by Delhi NCR (20 percent). Pune, however, saw the maximum rise of over 45 percent in property sales, QoQ, as it almost reached its pre-COVID sales figures with the absorption of about 9,600 housing units. Demand from the Non-Resident Indians (NRIs) went up significantly by over 200 percent since March 2020. Across the consumer segments, ready units remained the prime choice as growing liquidity constraints kept buyers wary and cautious of underconstruction projects.

Sales of ready-to-move residential projects spiked during Q4 2020 due to an improved sentiment towards owning a home. Demand for under-construction projects remained grim, barring those offered by financially stable real estate developers. The Centre’s assistance with stress funds for stuck realty projects may pave the way for those nearing completion in the ensuing quarters.

Despite an unrelenting focus on completing ongoing housing projects, a few Grade A developers launched new projects, sealing the sentiment of market revival. Across the top eight metro cities, approximately 400 housing projects (including relaunched projects and project phases) with over 26,700 units were launched. Mumbai took the lead and captured over 27 percent share of total new launches. Cumulatively, the unsold inventory levels grew marginally across the metro cities and stood at 4.62 lakh at the end of Oct-Dec 2020.

The average weighted prices across cities remained unchanged as the downward pressure of a perception-based slowdown forced developers and sellers to maintain status quo. However, with home loan interest rates continuing at a 15-year low, the Centre urging State governments to address the exorbitant stamp duty charges and pumping in funds to expedite the development of key infrastructure projects, the real estate sector is poised to register growth in the year 2021.

The affordable and mid-income price segment remained the most popular across cities. Several developers were seen realigning their projects and pricing as per consumer demand. Government, too, increased its focus on the affordable housing sector by introducing incentives for the rental complexes scheme and approving housing projects under SWAMIH Fund.

The rental landscape continued grim as professionals and students continued operating from their hometowns amid rising COVID cases. The new-found strain of the virus may prolong the reopening of the market for another quarter; dampening the rental scenario further across cities. However, the capital market is expected to continue growing on the back of end-user demand.