Ramesh Nair – CEO & Country Head, JLL India

By Ramesh Nair – CEO & Country Head, JLL India

Although leasing activity declined by 13% year-on-year in Asia Pacific in Q2, volumes were down only 2% in the first half of the year, indicating stable leasing levels across the region. Cities like Seoul and Taipei saw sluggish tenant demand impacting leasing activity. Delhi-NCR has continued to be the regional leader for leasing volumes while Bengaluru also came ahead of other active regional markets, including Guangzhou, Manila and Melbourne.

Higher levels of activity in Bengaluru (+11%) and Delhi-NCR (+14%) were, however, offset by lower levels of take-up in Mumbai (-23%) and Chennai (-53%). While Mumbai saw lower volumes in Q2 as a few big-ticket deals did not crystalize in time, Chennai suffered from lack of quality office spaces in a low vacancy market. Aggregate gross leasing for four of India tier-I cities registered a small 3% decline in H1 2017.

The first half of 2017 has seen take-up reach just under 10 mn sft across the four major cities, which is slightly less than H1 2016 when the take-up exceeded 10 mn sft. Traditional sectors remained the primary demand drivers but uncertainty surrounding US offshoring policy and automation has seen ITeS’ firms exercise caution. Co-working operators have started to be major contributors of space take-up.

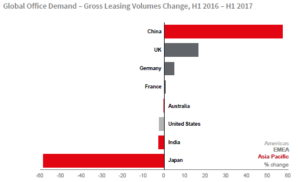

What happened in other leading markets?

Leasing activity was higher in all three China tier-I cities. Domestic financials, insurance, real estate and tech firms drove leasing activity across these markets. At the same time, Hong Kong has witnessed strong demand from financial firms from the PRC.

A lack of available space in existing buildings and upcoming supply in Japan’s core areas continued to impact leasing activity in the Grade A segment in the first half of the year.

Gross leasing volumes in H1 2017 in Singapore were notably higher than a year earlier, bolstered by large deals on recently completed or upcoming buildings as tenants take advantage of lower rents to lease high-quality space.

Aggregate gross leasing volumes in Australia during H1 2017 were flat on a year ago. Demand is strong and broadly-based in Melbourne (up 78% in H1), with centralisation a key theme. In Sydney, however, gross leasing was 33% lower than a year earlier due to a high base effect as leasing levels in H1 2016 were bolstered by pre-leasing in new developments.

Source: JLL, July 2017

Source: JLL, July 2017

(Based on 6 cities in Australia; 3 cities in China; 2 cities in France; 5 cities in Germany; 4 cities in India; 1 city (Tokyo) in Japan; 50 cities in the United States; 2 cities in the UK)

Overall, Asia Pacific leasing volumes this year are likely to be marginally lower (0% to -5%) than in 2016, with upside potential for improved activity by year-end.

Globally, however, office leasing activity has been remarkably stable during the first half of 2017, with global volumes virtually unchanged on the same period of 2016. For the full year 2017, we expect global leasing volumes to remain steady, matching the levels recorded in 2016. Volumes are projected to be somewhat higher than in 2016 in the United States, stable in Europe and slightly lower in Asia Pacific.